A 529 plan lets money grow and come out tax-free, but fees nibble at returns.

Direct-sold portfolios now charge as little as 0.05 percent, while some still exceed 1 percent—an 18-year gap worth thousands¹.

SECURE 2.0 adds a safety valve: starting with 2024 contributions, unused dollars can shift into the beneficiary’s Roth IRA, tax- and penalty-free².

Low fees plus new flexibility leave one mandate—choose the plan that gives every dollar room to grow.

Run your numbers with a quick college savings calculator, automate the draft, and move on.

Ready? Let’s make every basis point count.

How we chose the most affordable plans

We ranked every 529 plan by one question: how many of your dollars grow for your child instead of covering overhead?

Fees carried 60 % of the score because they tap the balance every year. We measured total asset-based cost, the fund expense plus any program or state charge. Plans above 0.25 % were cut.

Investment choice counted for 20 %. Age-based tracks for autopilot savers and single-fund options for hands-on parents both needed solid performance records. Usability earned 10 %. We opened sample accounts, tested enrollment, and noted minimums, autopay tools, and gifting portals.

The final 10 % rewarded sustainability. ESG or fossil-fuel-free portfolios at a fair price earned bonus points.

Our shortlist nearly matches Morningstar’s current Gold roster (Utah, Illinois, Massachusetts, Pennsylvania, and Alaska), proof that low cost and strong oversight go together, according to ratings published on my529.org.

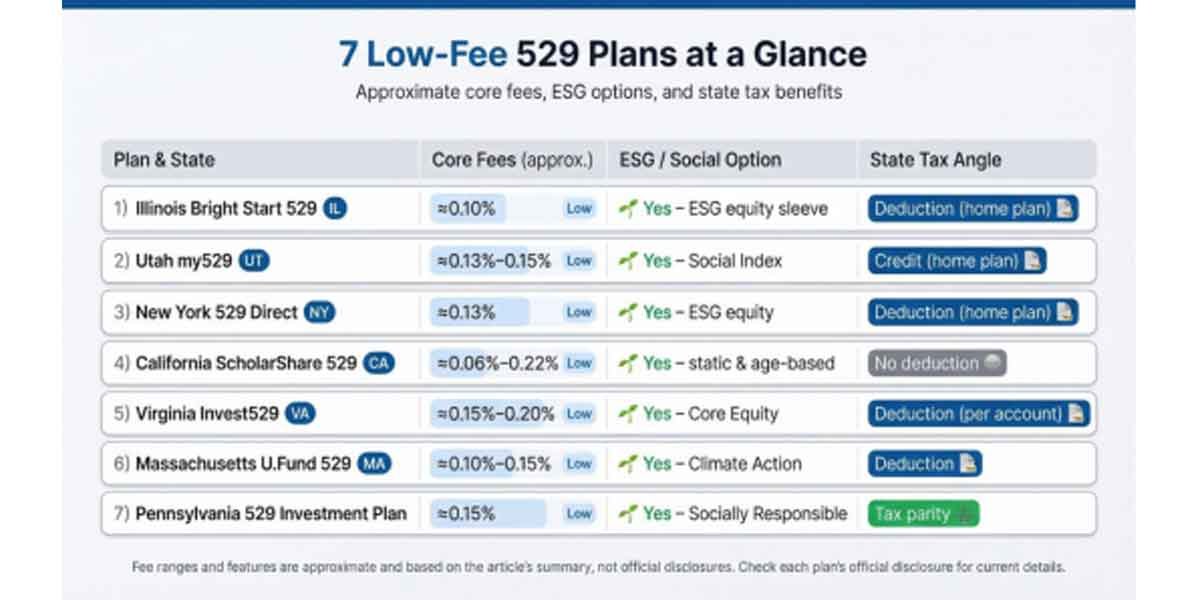

Only seven plans cleared every bar. They’re up next.

1. Illinois Bright Start 529: high ratings, ultra-low costs

Bright Start meets every key metric we track—fees, oversight, flexibility, and a concrete perk for in-state families.

Age-based index portfolios sit near 0.10 percent all-in, and even the actively managed tracks stay modest, so costs never overtake convenience.

Live in Illinois? Contributions lower state taxable income by up to ten thousand dollars for single filers or twenty thousand for joint returns. That benefit arrives in year one and compounds alongside market gains.

Investment choice is broad yet intuitive. Before locking in a track, families can calculate how much to save for college by entering a child’s age, an estimated tuition, and their expected rate of return; the tool then shows the monthly contribution required and how that figure changes with different portfolios. Then they can set and forget an age glide path, park assets in a single index fund, or choose the ESG sleeve powered by Parnassus Core Equity.

The interface feels modern, auto-pay setup takes minutes, and there are no maintenance fees.

Illinois Bright Start 529 Official Website Interface Screenshot

Bottom line: Bright Start lets every dollar grow, and Illinois residents enjoy an extra tax lift. Savers elsewhere still gain one of the cheapest, top-rated platforms with no residency rule.

2. Utah my529: lowest fees and DIY flexibility

Seasoned savers often point to Utah my529 when asked about the cheapest 529 plan.

Age-based tracks cost about 0.13 to 0.15 percent all-in, a figure that already covers Vanguard or DFA index funds. The program adds no extra fee and hides no fine-print charges.

If you prefer to build a portfolio yourself, my529 lets you choose individual index funds. You could keep everything in a Total U.S. Stock Market fund at roughly 0.12 percent, then add bonds or international stocks as college nears.

Eco-minded families can select the Social Index portfolio that tracks Vanguard’s ESG U.S. Stock Index at the same low price.

Utah residents receive a modest state tax credit, but the plan’s low fees attract investors nationwide. Enrollment is fast, the interface intuitive, and customer support earns frequent praise on parent forums.

Utah my529 Official Website Interface Screenshot

In short, my529 offers control and minimal cost in one package.

3. New York 529 Direct: Vanguard simplicity at a bargain

If you want investing to feel straightforward, New York’s direct-sold plan is a solid choice. Every portfolio uses Vanguard index funds, keeping costs low and the strategy clear.

Pick an aggressive, moderate, or conservative age track, and the plan gradually shifts to lower risk as college nears. Total expenses average about 0.13 percent, with no account or advisor fees.

Prefer to manage allocations yourself? Static portfolios let you hold a full stock position or create a custom stock-bond mix without extra cost.

An ESG equity option tracks the Vanguard FTSE Social Index at roughly 0.12 percent, giving socially responsible exposure without a price premium.

New York residents can deduct up to five thousand dollars of contributions each year, or ten thousand for joint filers. Low fees and Vanguard stewardship still attract savers nationwide, even when no local tax break applies.

Opening an account takes minutes, the minimum deposit is one dollar, and the dashboard stays uncluttered. Simple. Cheap. Effective.

New York 529 Direct Plan Official Website Dashboard Screenshot

4. California ScholarShare 529: low-cost index funds for everyone

ScholarShare seldom lands in headlines, yet its fee list is among the lowest we have found.

Single-fund index portfolios cost just 0.06 percent. Age-based tracks rise to about 0.22 percent, still below most competitors. California removed program and maintenance fees, so the posted cost is the total cost.

Because the state offers no tax deduction, residents can focus solely on merit. Choices include three age glide paths, a single S&P 500 fund, or a mix of static options.

Greener investors can pick a static ESG equity portfolio or the country’s only age-based ESG track. These options run around 0.45 percent.

The website feels clean, mobile deposits work smoothly, and the $25 opening minimum keeps entry easy. Parents on finance forums praise ScholarShare for combining Vanguard-level pricing with a TIAA interface.

If you want very low-cost index exposure through a simple portal and do not need a state deduction, ScholarShare deserves a look.

5. Virginia Invest529: low fees and lots of choice

Invest529 feels like a financial buffet: plenty of healthy staples, a few treats, and each option lists its price up front.

Index-based age tracks and static portfolios cost about 0.15 to 0.20 percent, matching our low-fee target. Virginia recently removed its small account fee, so nothing nibbles at returns.

Residents can deduct up to four thousand dollars per account from state taxable income each year, and unused amounts carry forward without limit. Even without that perk, the plan’s variety brings in savers nationwide.

Choose among several glide paths, single-fund index options, or an ESG Core Equity portfolio from Parnassus. The ESG choice costs around 0.55 percent, and selecting it is optional.

The portal is clean, the mobile app handles quick checks, and the gifting tool turns birthdays into contribution days with one link.

Invest529 proves you do not have to give up choice to keep costs low. Pick a simple index track for minimal pricing, or explore the wider lineup and still pay less than many rivals charge for basics.

6. Massachusetts U.Fund 529: Fidelity know-how, index-level pricing

The U.Fund pairs Fidelity’s broad investment lineup with costs that match index-only rivals.

Core portfolios, whether age-based or static, stay in the 0.10 to 0.15 percent range—impressive when a household name absorbs most administrative work.

Massachusetts residents receive a modest state tax deduction, and savers nationwide value the familiar Fidelity dashboard. You can view a 529 balance beside an IRA or brokerage account, then move cash between them in two clicks.

Climate-focused parents can choose the Climate Action portfolio. It costs about 1.05 percent, but the option lets greener savers stay on the platform.

Opening an account takes fifteen minutes, the minimum deposit is fifteen dollars with automatic drafts, and the gifting tool turns birthdays into contribution days.

If you already trust Fidelity or simply want big-firm resources at low fees, the U.Fund meets the mark.

7. Pennsylvania 529 Investment Plan: fee cuts and tax-parity power

Pennsylvania trimmed program fees in 2023, turning an already solid plan into a standout deal.

Most age-based and static portfolios now cost about 0.15 percent, keeping pace with Utah and Illinois. The state also removed its small annual account charge, so ongoing overhead is close to zero.

Residents benefit from tax parity: you can deduct contributions to any state’s 529, up to about 17,000 dollars per beneficiary each year, yet the home plan is now so affordable that shopping around is less necessary.

Investment choices center on Vanguard index funds. Choose an age glide path, a 100 percent equity option, or the Socially Responsible Equity portfolio at roughly 0.27 percent.

Opening an account is quick, minimums start at 25 dollars, and rollovers arrive without extra steps. The plan holds a Morningstar Gold rating, confirming that the fee cut reflects lasting stewardship.

Bottom line: PA 529 is a simple, low-maintenance option that rewards locals and welcomes everyone.

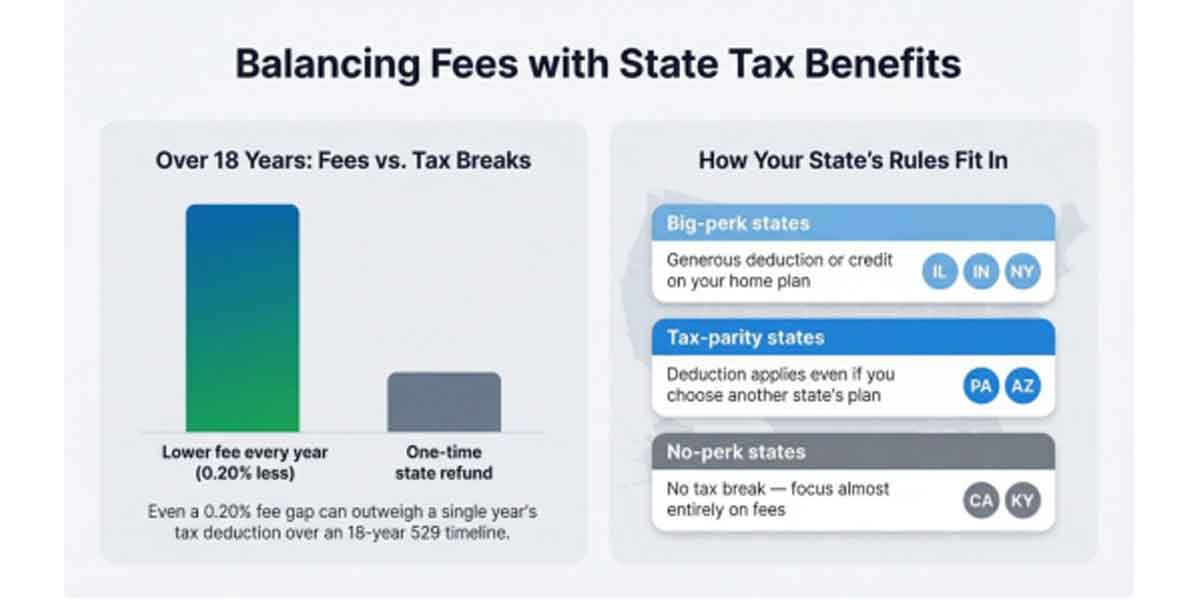

Balancing low fees with state tax benefits

Low fees compound year after year, while state tax deductions arrive as a one-time refund. Smart savers weigh both before choosing a 529.

First, confirm your state’s policy. Some states, including Illinois and Indiana, reduce taxable income each spring when you contribute. Others, such as California and Kentucky, offer no break, so fee savings carry more weight.

A deduction or credit applies only to new money added this year. Fees skim a slice of the entire balance every year. Over an 18-year timeline, even a 0.20 percent gap can outweigh a single tax perk.

Use this quick rule of thumb:

- Big-perk states (Indiana credit, Illinois deduction, New York deduction) can justify a home plan if fees remain low.

- Tax-parity states like Pennsylvania or Arizona let you claim the deduction while choosing any plan, so aim for the lowest cost.

- No-perk states should focus almost entirely on expense ratios and investment quality.

Check whether the deduction has an annual cap. If you plan to contribute beyond that limit, place the first portion in the home plan for the tax break and direct the rest to the cheapest option on our list.

This split approach keeps today’s refund in your pocket without sacrificing decades of growth.

FAQs: your smart-saver cheat sheet

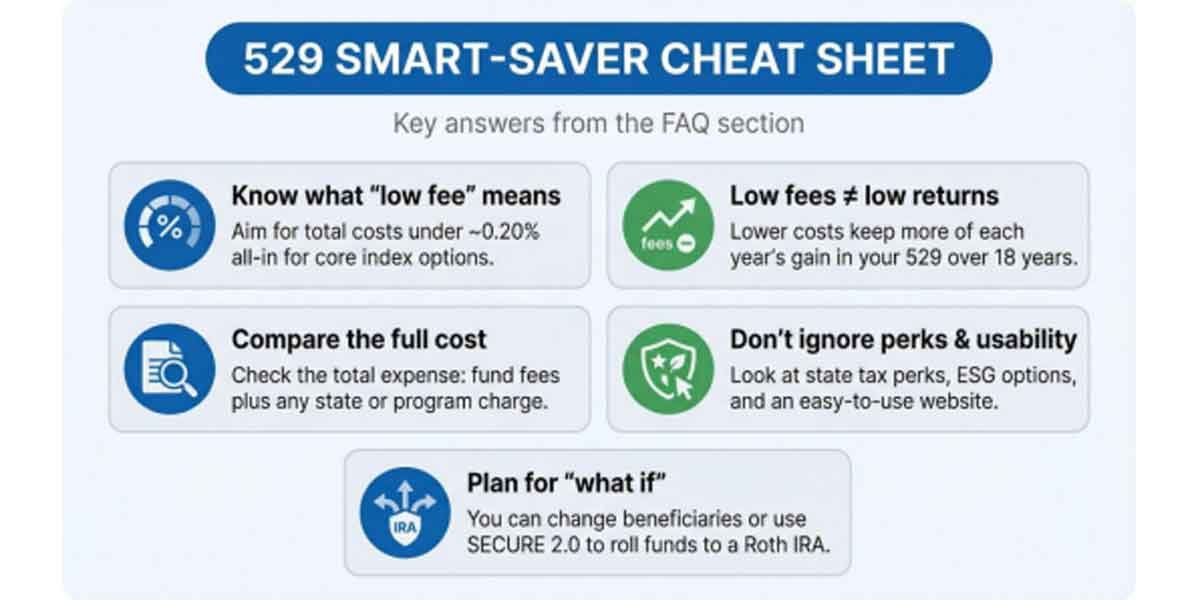

What counts as a “low” fee?

Anything under about 0.20 percent all-in ranks among the best. Every plan highlighted here keeps its core index lineup below that mark, while many older options cost three to five times more.

Do low fees hurt returns?

No. Lower cost means more of each year’s gain stays in the account. Over 18 years a 0.50 percent drag can erase thousands of dollars. That money could cover books or an entire semester of housing.

How can I compare plans quickly?

Find the total asset-based expense in each plan’s disclosure, then check for any state or program fee. Multiply the combined rate by a projected balance and the years until college; the cheaper plan will reveal itself in seconds.

Besides fees, what else matters?

State tax perks, investment choice, website ease, and customer service. Begin with cost, then see if a home-state deduction or an ESG option swings the decision.

What if my child skips college?

You can name a new beneficiary or, under SECURE 2.0, roll unused funds into the student’s Roth IRA within lifetime limits. This flexibility removes the old fear of saving “too much.”

How do I open an account?

Choose a plan, spend 15 minutes on the enrollment form, link a bank account, and schedule an automatic draft. Progress builds when deposits run on autopilot.

Conclusion

Small steps, low costs, big results. That is the 529 formula in a nutshell.